Paramount TPA Policy & Claim Status

Organization : Paramount Health Group

Service Name : Policy & Claim Status

| Want to ask a question / comment on this post? Go to bottom of this page. |

|---|

Check Status Here : https://www.paramounttpa.com/

How To Claim Paramount Policy Status?

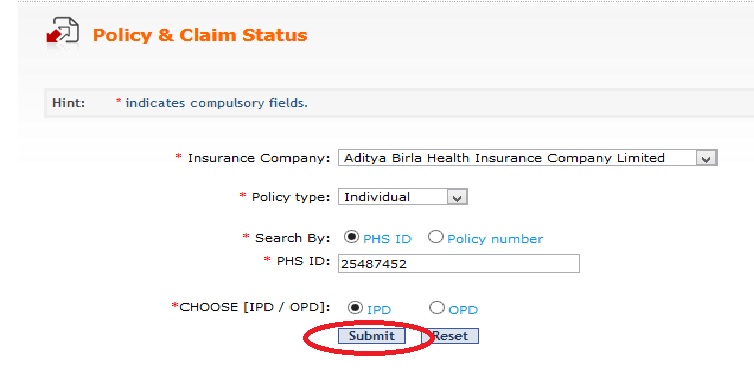

Select the Insurance Company & Policy type & Submit

Related : Paramount TPA Cashless & Reimbursement Claim Procedure : www.statusin.in/2940.html

** Select Insurance Company

** Select * Policy type:

** Select * Search By – PHS ID/ Policy number

** Enter * PHS ID Number

** *CHOOSE [IPD / OPD]

** Click on Submit button.

Policy Information:

Paramount Coverage

In the event of any claim becoming admissible under this scheme, the company will pay through TPA to the Hospital/Nursing Home or insured person the amount of such expenses as would fall under different heads mentioned below and as are reasonably and necessarily incurred thereof by or on behalf of such insured person.

A. Room, Boarding Expenses as provided by the Hospital/ Nursing Home.

B. Nursing Expenses.

C. Surgeon, Anesthetist, Medical Practitioner, Consultants, Specialists Fees.

D. Anesthetist, Blood, Oxygen, Operation Theatre Charges, Surgical appliances, Medicines & Drugs, Diagnostic Materials and X-ray. Dialysis, Chemotherapy, Radiotherapy, Cost of Pacemaker, Artificial Limbs & Cost of organs and similar expenses.

The claims admitted during the period of insurance shall not exceed the Sum Insured per person as mentioned in the schedule Expenses on ‘Hospitalisation for minimum period of 24 hours is admissible. However, this time limit is not applied to specific treatments, i.e., Dialysis, Chemotherapy, Radiotherapy; Eye Surgery, Dental Surgery, Lithotripsy (Kidney Stone removal), D & C,

Pre-Hospitalisation:

Relevant medical expenses incurred during period up to 30 days prior to Hospitalisation on disease / illness / injury sustained will be considered as part of claim.

Post Hospitalisation:

Relevant medical expenses incurred during period up to 60 days after Hospitalisation on disease/illness/injury sustained will be considered as part of claim.

Exclusions

1. All diseases/injuries, which are pre-existing when the cover incepts for the first time.

2. During the first year of the operation of the policy, the expenses on treatment of diseases such as Cataract, Benign Prostatic Hyperthrophy, Hysterectomy for Mennorrhagia, or Fibromyoma, Hernia, Hydrocele, Congenital internal disease,Fistula in anus, piles, Sinusitis and related disorders are not payable.

If these diseases (other than Congenital Internal Diseases) are pre-existing at the time of proposal they will not be covered even during subsequent period of renewal. If the Insured is aware of the existence of congenital internal disease before inception of the policy, the same will be treated as pre-existing.

3. Injury / disease directly or indirectly caused by or arising from or attributable to invasion, Act of Foreign Enemy, War like operations (whether war be declared or not)

4. Circumcision unless necessary for treatment of a disease.

5. Maternity Expenses

6. Cost of spectacles and contact lenses, hearing aids.

7. Dental treatment or surgery of any kind unless requiring hospitalization.

8. Convalescence, general debility; run-down condition or rest cure, Congenital external disease or defects or anomalies, Sterility, Venereal disease, intentional self injury and use of intoxicating drugs / alcohol.

9. All expenses arising out of any condition directly or indirectly caused to or associated with Human T-Cell Lymphotropic Virus Type III (HTLB- III) or Lymphadinopathy Associated Virus (LAV) or the Mutants Derivative or Variation Deficiency Syndrome or any syndrome or condition of a similar kind commonly referred to as AIDS.

10. Charges incurred at Hospital or Nursing Home primarily for diagnosis, X-ray or Laboratory examinations or other diagnostic studies not consistent with or incidental to the diagnosis and treatment of positive existence of presence of any ailment, sickness or injury, for which confinement is required at a Hospital / Nursing Home or at home under domiciliary hospitalisation as defined.

11. Expenses on vitamins and tonics unless forming part of treatment for injury or diseases as certified by the attending physician.

12. Injury or Disease directly or indirectly caused by or contributed to by nuclear weapon / materials.

13. Treatment arising from or traceable to pregnancy (including voluntary termination or pregnancy) and childbirth (Including caesarian section)

14. Naturopathy treatment.

FAQ On Paramount Policy

Here are some frequently asked questions (FAQ) about Paramount Policy

What is Paramount Policy?

Paramount Policy is a health insurance policy that provides coverage for a wide range of medical expenses, including doctor visits, hospital stays, and prescription drugs.

Who can get Paramount Policy?

Paramount Policy is available to individuals and families who meet certain eligibility requirements. These requirements vary depending on the type of policy you choose.

How much does Paramount Policy cost?

The cost of Paramount Policy varies depending on the type of policy you choose, your age, and your health status.

claim